Despite the relief, the macro backdrop remains complicated. Headline CPI rose to 4.2% in May, the highest reading since 2023, while core PCE, the Fed’s preferred underlying inflation gauge, increased to 3.4%. At the same time, the labor market remained resilient, with unemployment holding near 4.3% through May and initial jobless claims inching up to 215k in June. Consumer sentiment remained weak, falling to a record-low 44.8 in May before rebounding to 49.5 in June, still an exceptionally depressed level. The weakness in sentiment has not translated into weaker spending, with retail sales rising 0.9% month over month in May.

The Fed remains in a difficult position as economic signals continue to conflict. Kevin Warsh chaired his first FOMC meeting and emphasized the Fed’s commitment to price stability while removing much of the forward guidance investors had grown accustomed to under prior regimes. The Fed held rates steady at 3.50% to 3.75%, but markets focused on the updated dot plot, which showed a meaningful shift toward additional tightening by year-end.

-----------------------------------------------------------------------------------------------------------------------------------------------------

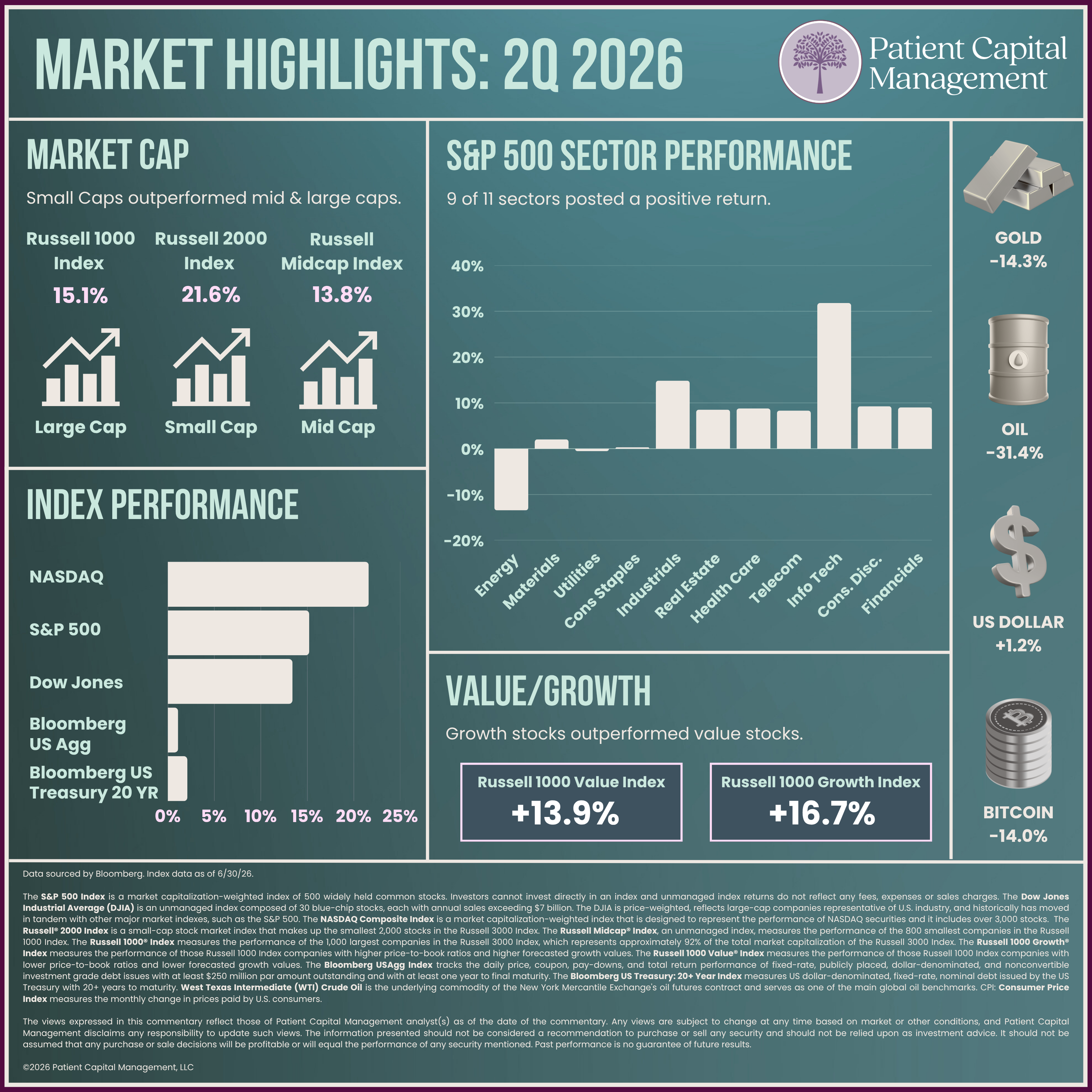

All major equity indices reached new all-time highs during the quarter. The Nasdaq Composite led the major benchmarks, advancing 21.6%, followed by the S&P 500, which gained 15.2%, and the Dow Jones Industrial Average, which rose 13.4%. Nine of the eleven sectors within the S&P 500 posted positive returns. Information Technology led, surging 31.8%, followed by Industrials and Consumer Discretionary, which returned 14.9% and 9.3%, respectively. Energy gave back some of its first quarter gains declining 13.4% as crude oil prices softened.

Small-caps led this quarter, with the Russell 2000 gaining 21.6%, its 8th best quarter since inception, outperforming both large-caps and mid-caps. The Russell 1000 rose 15.1% and the Mid-Cap Index posted returns of 13.8%. Growth regained the lead, outperforming value, with the Russell 1000 Growth Index rising 16.7% while the Russell 1000 Value Index returned 13.9%.

Bonds were positive but underperformed all equity indexes in the quarter. Long-dated US Treasuries returned 2.1% followed by US Corporates with the Bloomberg Aggregate returning 1.1%.

The U.S. dollar gained 1.2% during the quarter, while gold fell 14.3%, breaking below its 200-day moving average for the first time since the third quarter of 2023. West Texas Intermediate (WTI) pulled back 31.4% but remains up 21.0% year-to-date. Bitcoin extended its losing streak to three consecutive quarters, falling 14.0% to end the quarter at $58.6k.

Data sourced by Bloomberg. Index data as of 06/30/26.

The S&P 500 Index is a market capitalization-weighted index of 500 widely held common stocks. Investors cannot invest directly in an index and unmanaged index returns do not reflect any fees, expenses or sales charges. The Dow Jones Industrial Average (DJIA) is an unmanaged index composed of 30 blue-chip stocks, each with annual sales exceeding $7 billion. The DJIA is price-weighted, reflects large-cap companies representative of U.S. industry, and historically has moved in tandem with other major market indexes, such as the S&P 500. The NASDAQ Composite Index is a market capitalization-weighted index that is designed to represent the performance of NASDAQ securities and it includes over 3,000 stocks. The Russell® 2000 Index is a small-cap stock market index that makes up the smallest 2,000 stocks in the Russell 3000 Index. The Russell Midcap® Index, an unmanaged index, measures the performance of the 800 smallest companies in the Russell 1000 Index. The Russell 1000® Index measures the performance of the 1,000 largest companies in the Russell 3000 Index, which represents approximately 92% of the total market capitalization of the Russell 3000 Index. The Russell 1000 Growth® Index measures the performance of those Russell 1000 Index companies with higher price-to-book ratios and higher forecasted growth values. The Russell 1000 Value® Index measures the performance of those Russell 1000 Index companies with lower price-to-book ratios and lower forecasted growth values. The Bloomberg US Treasury: 20+ Year Index measures US dollar-denominated, fixed-rate, nominal debt issued by the US Treasury with 20+ years to maturity. The Bloomberg USAgg Index is a broad-based flagship benchmark that measures the investment grade, US dollar- denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate pass-throughs), ABS and CMBS (agency and non-agency). West Texas Intermediate (WTI) Crude Oil is the underlying commodity of the New York Mercantile Exchange's oil futures contract and serves as one of the main global oil benchmarks. CPI: Consumer Price Index measures the monthly change in prices paid by U.S. consumers. PCE: Personal consumption expenditures includes a measure of consumer spending on goods and services among households in the US. PCE, CPI, and inflation rates based on available data at the time the piece was written and are not guaranteed to stay the same in the future.

The views expressed in this commentary reflect those of Patient Capital Management analyst(s) as of the date of the commentary. Any views are subject to change at any time based on market or other conditions, and Patient Capital Management disclaims any responsibility to update such views. The information presented should not be considered a recommendation to purchase or sell any security and should not be relied upon as investment advice. It should not be assumed that any purchase or sale decisions will be profitable or will equal the performance of any security mentioned. Past performance is no guarantee of future results.

©2026 Patient Capital Management, LLC

Share