This presentation quickly grabbed my attention since discounted cash flow valuations (DCF) are a major part of our process. We focus on the cash flow generation of companies and believe that a company’s value is the Present Value of its expected future free cash flows. As an example of relevance, Professor Damodaran has written a number of pieces on Valeant Pharmaceuticals (VRX), one of our holdings, with the most recent piece valuing the company at $27, implying an upside of 72%. Our valuation of Valeant is more optimistic, as we believe the stock can compound at 20-25% annually for the next 5 years.

According to Prof. Damodaran, the Ten DCF Myths:

- D + CF = DCF

- A DCF is an exercise in modeling & number crunching.

- You cannot do a DCF when there is too much uncertainty.

- The most critical input in a DCF is the discount rate and you have to believe in beta, to use the discount rate.

- The biggest number in a DCF is the terminal value and it is unbounded.

- A DCF requires too many assumptions and can be manipulated to yield any value you want.

- A DCF cannot value brand name or other intangibles.

- A DCF yields a conservative estimate of value. It is better to under estimate value than over estimate it.

- A DCF is static. It is pointless in a dynamic world.

- A DCF is an academic exercise.

While all ten myths are important to understand when creating a DCF, the two I found most interesting were #2 and #6 because they brought to light the ability for biases to creep into modeling. Previously, I had written about my experience witnessing behavioral biases in action in early 2016, but I had not realized how prevalent biases are in models as well.

#2 A DCF is an exercise in modeling & number crunching

Throughout life, you hear people refer to themselves as either “number people” or “story people” but this implies that there is a clear divide between numbers and narrative. While traditionally we might think of investing as a “numbers person” game this type of thinking is changing. Many researchers, such as Professor Damodaran, believe that good valuations must use numbers that are connected to a narrative otherwise you can end up with a valuation that is too good to be true (i.e. a retailer growing 25% a year while only reinvesting 1% a year).

Narratives provide a basis for the estimates that analysts use in a DCF (growth rate, operating margins, reinvestment rate, etc.) The narrative feeds directly into the numbers and each narrative will result in a different valuation outcome. A good example of how different narratives can result in drastically different valuations is Damodaran’s valuation of Uber using his narrative versus Bill Gurley’s, one of the best tech venture investors, narrative.

| Uber (Bill Gurley) | Uber (Bill Gurley Modified) | Uber (Damodaran) | |

| Narrative | Uber will expand the car service market substantially, bringing in mass transit users & non-users from the suburbs into the market, and use its networking advantage to gain a dominant market share, while maintaining its revenue slice at 20% | Uber will expand the car service market substantially, bringing in mass transit users & non-users from the suburbs into the market, and use its networking advantage to gain a dominant market share, while cutting prices and margins (to 10%) | Uber will expand the car service market moderately, primarily in urban environments, and use its competitive advantage to get a significant but not dominant market share and maintain its revenue slice at 20% |

| Total Market | $300B, growing at 3% a yr | $300B, growing at 3% a yr | $100B, growing at 6% a yr |

| Market Share | 40% | 40% | 10% |

| Uber's Revenue Slice | 20% | 10% | 20% |

| Value for Uber | $53.4B + option value of entering car ownership market ($10B+) | $28.7B + option value of entering car ownership market ($6B+) | $5.9B + option value of entering car ownership market ($2-3B) |

Source: Aswath Damodaran. Presentation at the CFA Institute Conference on Equity Research and Valuation

As you can see, the valuations are drastically different but each one is the result of different assumptions related to the different stories being told about the company’s future.

However, just having a story alone does not make it a good valuation as narratives are subject to biases. The narrative must be tested to make sure that it is possible, plausible and probable to help avoid any runaway stories (Professor Damodaran uses the example of Theranos). As Professor Damodaran says, “there are a lot of possible narratives, not all of them are plausible and only a few of them are probable”. Testing a narrative for the 3 P’s can help avoid some inherent biases when valuing a company. On his blog, Professor Damodaran talks about how it is not probable that Apple can grow 15% a year when 70% of their revenue is derived from smartphone sales which as an industry is only growing 3-5% a year (the market agrees since it implies revenue declines for Apple). Since the narrative has a large impact on the outcome of the valuation, it is important to try to minimize the biases that are present.

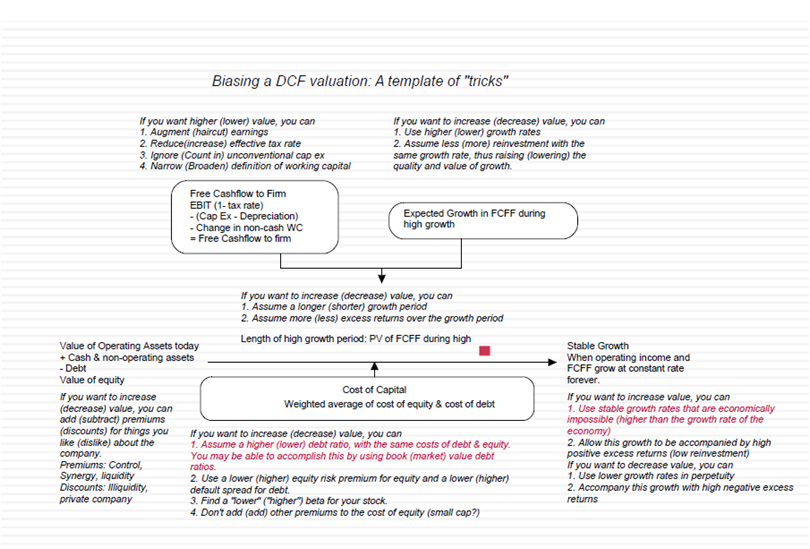

#6 A DCF requires too many assumptions and can be manipulated to yield any value you want

As we saw with the example above, different narratives will provide different valuations but as long as the numbers match the narrative and the narrative passes the 3 P’s test you will still have a useful valuation. A red flag would go up if you ended up with Professor Damodaran’s valuation of $5.9B by using Gurley’s narrative. For that to be possible there would have to be some serious manipulation in the model and the estimates you used could not possibly match the narrative. However, less obvious manipulations occur all the time in DCFs as a result of biases. The inherent problem with valuation is that valuations are usually done after an analyst is already familiar with a company, and has preconceived notions about its future and what they believe the company is worth. These biases can appear in a number of different parts of a DCF as Damodaran shows (see below - click the image to zoom).

Source: Aswath Damodaran. Presentation at the CFA Institute Conference on Equity Research and Valuation

While you can never fully remove biases from valuation, Professor Damodaran believes that you can decrease the impact of biases by being honest about what biases you might have and trying to minimize your exposure to factors that might increase your bias (i.e. avoid using management’s estimates of earnings/cashflows).

Attending conferences and hearing people like Professor Damodaran speak, is one of the ways we seek to improve our process and stay up to date on the newest research. Since attending the conference, I have looked to Professor Damodaran’s website to further expand my understanding of his philosophy and apply those insights into our modeling. Valuations and models are just another aspect of investing that is vulnerable to individual biases and by understanding these ten myths hopefully we can become more aware of them and work to minimize their impact.

The views expressed in this report reflect those of the LMM LLC (LMM) as of the date published. Any views are subject to change at any time based on market or other conditions, and LMM disclaims any responsibility to update such views. The information presented should not be considered a recommendation to purchase or sell any security and should not be relied upon as investment advice. It should not be assumed that any purchase or sale decisions will be profitable or will equal the performance of any security mentioned. Past performance is no guarantee of future results.

©2017 LMM LLC. LMM LLC is owned by Bill Miller and Legg Mason, Inc.

Share